Federal Reserve officials have recently been talking up the case for starting the process of tapering the central bank’s asset purchases. This baby step towards a more hawkish policy stance could begin as early as next month.

“While there is still room to improve on the employment leg of our mandate, I believe we have made enough progress such that tapering of our asset purchases should commence following our next FOMC meeting [Nov. 2-3],” Fed Governor Christopher Waller said earlier this week.

The reasoning is increasingly due to rising inflation pressures, even if Fed officials are downplaying that factor. But there’s an offsetting feature lurking: slower growth.

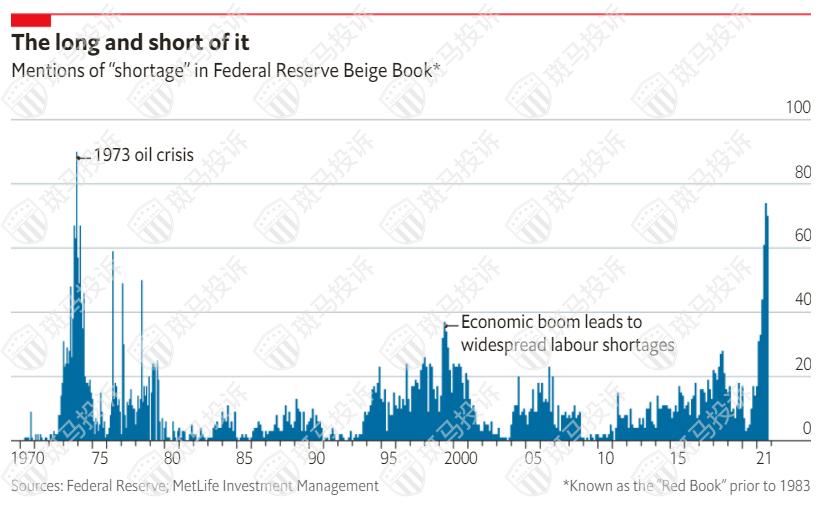

As reported here, there are signs that the economic rebound’s deceleration is picking up speed. Notably, the Atlanta Fed’s revised nowcast for the next week’s third-quarter GDP report has fallen sharply to a stall-speed 0.5% increase. Other estimates of Q3 growth are higher, but overall there’s a greater consensus among economic analysts and models that forward momentum for US economic activity is facing stronger headwinds. A key reason: shortages of goods and workers.

US economic activity is at risk of coming to a “screeching halt,” the owner of home-building firm in Florida told Congress this week. “Trying to schedule material deliveries has become almost impossible.”

The Fed is well aware of the shortages and, in fact, is talking about it. Mention of the word “shortage” in the central bank’s Beige Book, a regularly published summary of economic conditions, has surged recently, The Economist reports.

Although recession risk is still low, based on data published to date, economic activity looks set to slow for the near term, which could create new doubts about the wisdom of launching a hawkish shift in monetary policy.

To be sure, the market continues to price in low expectations for a rate hike through the first quarter of 2022, based on Fed funds futures. But a formal announcement of tapering next month would send a clear signal that the central bank is officially moving in that direction.

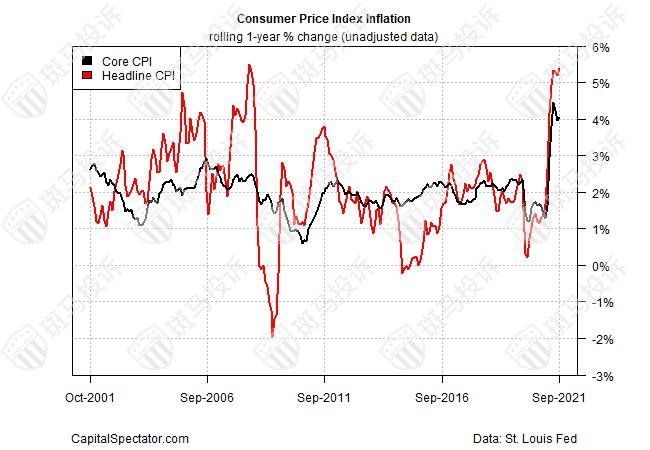

The surge in inflation is surely putting pressure on the Fed to start moving away from its pandemic-driven stimulus posture. Consumer price inflation is now running far above the Fed’s 2% target. The central bank’s official line is that higher pricing pressure is still transitory, but there’s stronger evidence that the process of peaking inflation could last longer than previously expected, raising the thorny question: How long is too long?

Richmond Federal Reserve President Thomas Barkin admitted as much last Friday, telling CNBC: “I do think there’s risk on the inflation side, and I’m watching that very carefully.”

It’s unclear if higher inflation will convince the Fed to start tapering next month or delay the decision due to signs of softer economic growth. But in a sign of the times, Fed Governor Waller opened the door to that possibility in comments earlier this week: “Of course, if economic conditions and the outlook were to deteriorate significantly, we could slow or pause this tapering.”

Meanwhile, there’s still widespread agreement at the Fed that inflation is transitory, which gives the central bank cover for deciding to delay any tapering decision without invoking growth concerns. But as uncertainty rises on the inflation and growth aspects of the outlook, the risk of a policy mistake is rising.

If inflation stays hot and the economy continues to cool, an ill-timed policy decision is more likely than not. The question is: Where is the greater risk: letting inflation run hot without trying to contain it, or prematurely squeezing policy just as the economy is moving into what could be an extended soft patch—or recession, according to some economists.

Making monetary policy decisions in real time is always challenging. That’s the nature of the beast in central banking, for some obvious reasons: relying on lagging economic data with effects that take months, or even years, to show up in the economy. The key difference this time: the challenge is higher than usual as economists struggle to sort out where the real risks lie.